-

15% Uncertainty: Greece, Europe and the tariff shockwave

15% Uncertainty: Greece, Europe and the tariff shockwave

-

Summit of transactions – Erdogan and Trump

Summit of transactions – Erdogan and Trump

-

Podcast - DETH and taxes: The only things certain in Greek politics

-

How will Trump's tariffs affect Greece?

How will Trump's tariffs affect Greece?

-

Podcast - Subsidise this: Fraud scandal delivers new blow to Greek PM

-

Fet-a-ccompli: Tariffs and Greece’s big cheese

Check, please: How much Alexis Tsipras's first months cost Greece

This time last year, Alexis Tsipras was in the awkward position of having missed his main objectives and found himself at odds with Greece’s creditors over his decision to hand out a 13th pension.

The conflicting interests of key stakeholders in Greece’s programme did not converge and the last Eurogroup of 2016 did not lead to the conclusion of the second review. Instead, it dragged on until June this year. Most critically, the main goal of being included in the European Central Bank’s QE programme was missed as the ECB required assurances about the country’s long-term debt sustainability and Germany was not willing to discuss even the medium-term debt relief measures, which were eventually pushed back to the end of the programme in 2018.

The months that followed were ridden with uncertainty and the economy slowed down. To seal a deal at last June’s Eurogroup, Tsipras agreed to additional fiscal measures worth 2 percent of GDP in the form of pension cuts and tax hikes for 2019 and 2020, mostly to appease the fiscal concerns of the International Monetary Fund.

Fast forward one year, and Tsipras has secured a staff-level agreement (SLA) on the third review and the big prize of exiting the memorandum era, which he promised Greeks in 2014 when he campaigned for their vote, is now in sight.

For Tsipras, it is probably the last opportunity to form a narrative that will preserve, or even restore some of his political capital and allow him to remain a key player in Greek politics. Greece has returned to growth. It has also managed to tap the markets twice, even in the form of bond swaps, with more issues to follow in the next months. The SYRIZA leader will claim that he was the one that managed to take Greece out of the MOUs, albeit with a delay.

However, can Greece’s prime minister really claim victory or feel vindicated about his strategy? Was the path that Tsipras mapped out the necessary route for Greece to reach the point of graduating from the ESM programme? What was the actual price for the tumultuous first half of 2015 that sealed the country’s fate?

What follows is a look at key aspects that were impacted by Tsipras’s negotiations, and the cost of each.

Economy

In 2014, Greece managed to record its first year of real growth since 2007. The economy grew by 0.7 percent that year. In Q3, it expanded by 1.3 percent compared to the previous year, which was one of the highest growth rates in the eurozone.

Greece was not out of the woods by any means. The budget was not performing according to targets and it ended up missing the programme’s primary surplus goal by a wide margin. The fifth review was demanding: the troika was expecting hard-to-swallow measures from Prime Minister Antonis Samaras and was offering little on the debt front.

Fiscally, the country had to agree to a path that would lead it to a primary surplus of 4.5 percent of GDP by 2016. Lacking the necessary votes in Parliament to elect a new President of the Republic, Samaras knew he was on borrowed time before national elections would be called.

Despite this complicated mix, if one leaves the political risk aside, Greece was expected to carry on growing in 2015 and 2016 even by the more conservative organisations. The Organisation for Economic Cooperation and Development, for instance, has been consistently the most reserved in its forecasts for Greece throughout the crisis.

In its economic outlook in the summer of 2014, it estimated that the economy would grow by 2.3 percent in 2015 and a further 3.3 percent in 2016.

The IMF is often inaccurate in its projections but cannot be accused of being overly optimistic with its estimates after 2012. In the last completed review document it put together in the summer of 2014, it expected Greece to grow by 2.9 percent in 2015 and 3.7 percent in 2016.

Both organisations saw private consumption and investments pick up due to the low base effect and having been suppressed from seven years of deep crisis at the time.

Going by the counterfactual, as Greece would need to deliver a big volume of fiscal consolidation to meet the 4.5 percent target, and by the experience we now have that investments have not been as responsive as initially hoped, it can be argued that both of those estimates required everything to work like clockwork and were probably too optimistic.

At the same time, Greece this year will manage to deliver growth of 1.6 percent, expected to accelerate to 2.5 percent in 2018, which shows that giving the economy a clean run without uncertain factors allows it to deliver growth despite the fiscal effort.

The argument that Greece would be in a position to deliver decent growth rates from 2015 onwards is supported by the fact that while Tsipras’s calamitous negotiating strategy was unfolding, the Greek economy did not tank in the first half of 2015 and it was only after the imposition of capital controls at the end of June 2015 to stave off an intense bank run that the economy contracted. Even then, it only shrank by 2.4 percent compared to a year earlier, mostly due to the fact that Greeks had anticipated developments and cash in circulation in the economy had reached an all-time high of 50.5 billion euros.

We estimate that in the 2015–2017 period Greece could have delivered average annual growth rates above 1.5 percent, not factoring in the potential inclusion in QE had Greece’s place in the eurozone not been put at risk during Tsipras’s first months in power.

The opportunity cost for the economy because of these developments in 2015 comes to approximately 10 billion euros.

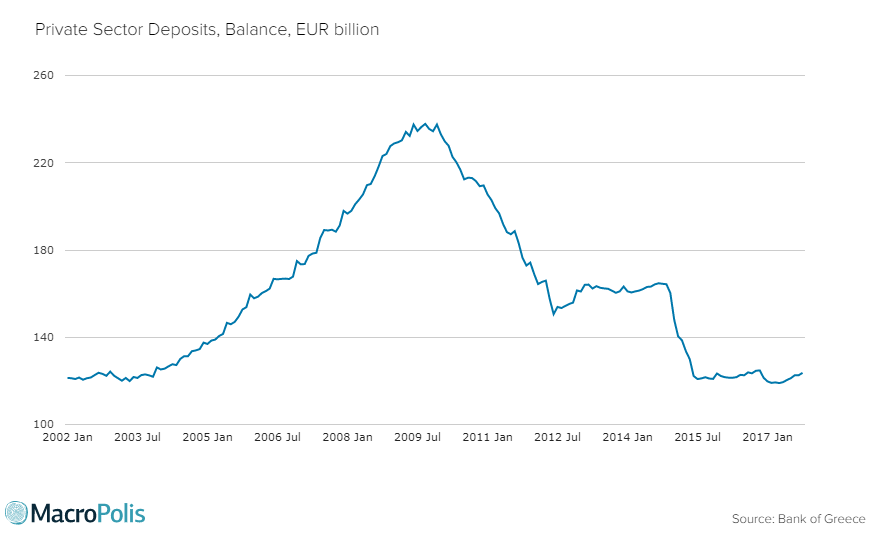

Banks

The Greek banks have been the barometer of Greece’s instability since the start of the crisis. When the crisis started, the private sector deposit base stood at 237.5 billion euros. The first wave of decline stopped in June 2012, when deposits landed at 150.6 billion. Following a modest recovery after Samaras formed a three-party coalition, deposits climbed back to roughly 164 billion in November 2014. At that point, it became apparent that Tsipras would trigger new elections by refusing to agree with the government’s proposal for a candidate in the presidential ballot scheduled for March 2015.

What followed was the sharpest drop in private sector deposits seen during the crisis. Deposits plummeted to 122.2 billion by June as Greeks were hoarding cash or moving it abroad in fear of a euro exit or in anticipation of capital controls after events in Cyprus

At the start of the crisis, the banking sector lost 87 billion euros of deposits in a 30-month period. In Tsipras’s tenure during the first half of 2015, the system lost roughly half that amount.

This puts Tsipras’s cost with regard to the banks deposit base at 42 billion euros.

Banks valuations

The Greek state, via the Hellenic Financial Stability Fund (HFSF), has contributed a total of 30.43 billion euros for the recapitalisation of the four core Greek banks. Of this, 25 billion was injected in the first round and 5.43 billion in the third round of the recap process. The latter is split between 1.36 billion in the form of shares and 4.07 billion in CoCos for two banks.

This is by far the largest financial commitment the Greek state has made in its history, representing close to 18 percent of the Greek economy. If you add the amounts that were required for the resolutions of banks, the total allocation reaches close to 44 billion euros, or a quarter of Greece’s economy.

At the end of 2013, the value of the holdings of HFSF in the Greek banks was worth roughly 22.6 billion euros.

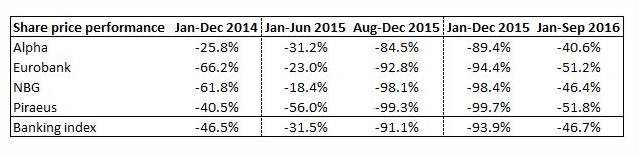

In 2014, the banking index tumbled by 46.5 percent, largely reflecting a nosedive of 33.7 percent in the last quarter of that year. The market started pricing in the uncertainty as Samaras and his government started rolling back reforms following defeats in local and European Parliament elections, failed to close the programme’s fifth review and national elections at the beginning of 2015 seemed inevitable.

The valuation of HFSF’s bank portfolio by the end of 2014 had nearly halved from a year earlier to just 11.6 billion.

If the end of 2014 was bad, the first year of Tsipras in power for banks valuations was catastrophic. In the first five months of the Tsipras administration, bank shares fell by another 31.5 percent on the back of the drawn-out and confrontational negotiations with creditors, deposit flight and further deterioration of the loan portfolio.

Bank shares slumped by another 91 percent by the end of the year. The share collapse in the second half of the year was marked by two key developments.

The banking index plummeted by 58 percent in the first five sessions after the five-week bank holiday that followed the imposition of capital controls in the wake of uncertainty about economic developments and rumours of massive additional capital needs.

Moreover, Greek bank shares plunged by 77.2 percent in the course of November 2015, when the share capital increases were announced and conducted, with deep discounts in the offer prices of the book-building processes.

Those discounts ranged from 34.4 percent for Alpha to 52.4 percent for Eurobank, up to 80 percent for Piraeus and a massive 93.8 percent for NBG. They were applied to the already low prices that resulted following a 74 percent nosedive of bank stock prices in the three-month period after the imposition of capital controls and before stress test results were announced by the Single Supervisory Mechanism on October 31.

Overall, the value of the Greek banking index was essentially wiped out during 2015, when it nosedived by 93.9 percent. This caused massive valuation losses for all bank shareholders, including the HFSF.

In 2015 alone, the cost of Tsipras’s management of the negotiations and subsequent recaps stands at 9 billion euros. If his share of responsibility for the events at the end of 2014 is also attributed, the bill rises to 12 billion euros.

State arrears

One of the immediate results of Tsipras’s choice to take the negotiations to the wire was the absence of disbursements from Greece’s official creditors, which led to a significant funding and liquidity squeeze for his government.

The Finance Ministry had to postpone or delay a large part of non-payroll costs from March 2015 to cover its imminent external funding needs.

State arrears to the private sector had peaked at 8.8 billion in 2012 but assisted by programme funding, they dropped back to 3 billion euros at the end of 2014.

By July 2015, arrears had reached 4.96 billion euros, a rise of 64 percent in just seven months. We attribute this effect fully to the acrimonious negotiations with the creditors, at a cost of nearly 2 billion euros.

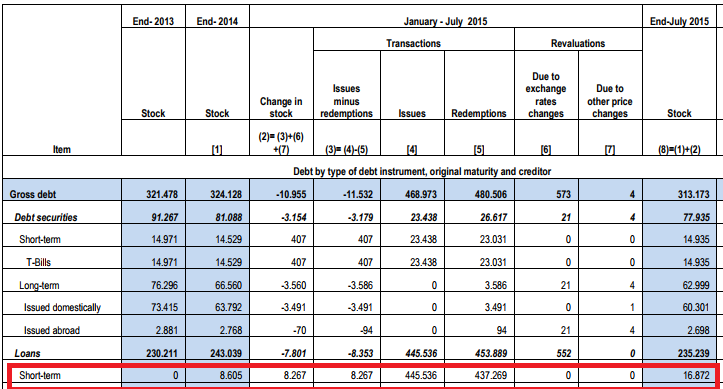

Repos

The Greek state had started using repos of the cash reserves from various state bodies in 2014 as a form of cash management to meet short-term funding needs. They were usually short-term transactions of 90 days or less that were either wound up or rolled over.

By the end of 2014, the stock of repos stood at 8.6 billion euros.

As a result of the liquidity squeeze that the SYRIZA-led government experienced in the first half of 2015, it resorted to using state bodies’ cash reserves not only as a short-term cash management solution but also as the necessary means to meet external obligations.

The stock of repos at the end of July 2015 had nearly doubled to 16.9 billion euros. The indication that Tsipras has not been able to return these funds to the state bodies is that the stock of repos in October of this year, almost 2.5 years since the peak, still stands at 16.5 billion euros.

The cost of the first half of 2015 on state cash comes to 8 billion euros.

The final bill

Tsipras has often had to contend with claims that he cost Greece 100 billion euros, which is the sum that some attach to the tenure of Yanis Varoufakis at the Finance Ministry. But this accusation is not justified. Even if the programme reaches its full capacity, which now seems unlikely as it is estimated there will be around 20 billion euros to spare, much of the financing was mostly used to meet debt obligations and Greece would have had to find the means to refinance these obligations anyway. Since it is locked out of the international markets, this financing could only come from the European Stability Mechanism.

Greece’s debt since the first quarter of 2015 has grown by 17 billion and not by 100.

However, the collateral damage of the first six months of 2015, which exceeds 70 billion euros, cannot be disputed and given the size and multitude of the costs, the logical question is whether it was all worth it.

Tsipras has very little to show in terms of substance for his combative stance. The framework remained the same as before, he did not get anything on debt relief and the revised programme targets were something that could have been achieved without testing his relationship with the eurozone. If anything, the complete collapse of trust from the other side of the table required him to make heavier commitments, like the asset development fund. Also, with regards to the fiscal effort, what was saved in terms of the targets had to be compensated by more heavy lifting due to the decline in economic activity.

Greece has been let down on numerous occasions by its politicians and Tsipras has often criticised opposition parties for their role that led to the crisis in 2009 and its management subsequently.

However, he must look back at those six months of 2015 and wonder what he was thinking. Even if his claim that he was acting with good and pure intentions is true, when you are in charge, you are measured against the outcome. This is why he is destined to find himself in the same group of politicians that he built his political career criticising: those that caused Greece severe damage.

7 Comment(s)

-

Posted by:

This article will prove that Greece was far better off as it has become the 17th Bundes-state of Germany. According to the shift in GDP in even the worsest area’s of Germany, Greece missed some 25.000 euro per capita.

The reason ? Germany is a transfer-union where difficult parts of the country are subsidised by the richer.

However, Greece is a souvereign nation in structural economic troubles and the EU is NOT a transfer-union.

Tsipras is doing his best to pokerplay with the Euro-group. But in poker, even the worst player can win when he has the deepest moneybag. Helas, Tsipras is one of the few players starting with a initial debt.

Two choices : stop playing and take the wrong ideas of the rich man at the table for grant. Or play and loose at the end, anyhow.

There was no win-win. There was only the pre-supposed liquidation of a left government in Athens.

This has nothing to do with economics, nor gdp’s or even capital.

The same “austerity”-politics costed in Holland approx. 8% of the GDP over the full nine years. No politician cares.

For you cannot calculate real economics before it happens in reality. In the hindsight, everybody, every country, too, could have done better.

So, its just a political question to sell this kind of aftermath stories. Tsipras was consequent to believe in the EU as a democratic and liberal partnership, being helpfull in a humane way.

It may be naive, but a few month later the ECB made a debt -construction of trillions, buying back outstanding obligations and loans. Who cares where the debt was in the book-keping of the EU ? A black hole, for ever gone.

I’m sure the Varoufakis plan to start a shadow economy with vouchers, would have been far better for Greece.

Try to calculate this alternative, if you dare !

For us, in the richer core-state of the Union, the Greece excercition according the ‘principals’ of the EU-EUROgroup showed, there was no such thing as solidarity and humane reason i -

Posted by:

This is a very partial analysis i am afraid. It postulates that the blame sits squarely on the Greek side - as if the Greek economy has not suffered due to politically induced asphyxiation from Germany - as if, the process was apolitical.

More importantly the analysis does not acknowledge that the unsuccessful battle with Greece's creditors took place on the basis that the imposed conditions were not sustainable. So in order to critique the losses suffered during the early months of Tsipras government you must make the highly problematic assumption that Greece was given a sustainable alternative.

Please do not let political processes be presented as economic forces. -

Posted by:

The 100 Bil. euro number has been thrown around by the opposition and is based on ignorance because expiring/maturing debts need to be recycled regardless. So the opposition, which is not known of any particular financial brilliance, has chosen to erroneously equate a line of credit to a net cost to the economy. This laughable position shows that modern finance is not understood by the great majority of Greek citizens and is particularly incomprehensible by its political class.

-

Posted by:

I'm sorry, but this looks completely wrong. GDP cost isn't 10 billion! You shouldn't just compare 2017 actual-world-GDP (A-GDP) with 2017-alternative-universe-GDP (ALT-U-GDP). You need to compare consensus long term growth trajectory forecasts now with ALT-U forecasts. Or, at the very least, you need to apply a discount rate to calculate losses in present value terms. So, for example 2018 A-GDP will be 100+2%, or whatever, while 2018 ALT-U-GDP would be 110+2.5% or whatever. Then for 2019 compare 2018 ALT-U-GDP + ALT-U consensus growth forecast with consensus-projected 2018 A-GDP+ consensus growth forecast. Do the maths for, say, a generation's life span, our generation, and then you ll have the actual cost. That would be a much more accurate estimate than adding real GDP to arrears (!), i.e apples and oranges, to come up with a cost.

-

Posted by:

Thanks, we have made a conscious effort to avoid the apples and oranges situation and this is why we have not aggregated in the piece, we present the cost on different aspects that were affected by the first half of 2015 and that is also to first degree due to space limitations. Also the impact on the economy is clear for the 2015 - 2017 period, i,e, where we would be now had Tsipras not chosen this path. Happy to include a reference in the piece if you do the longer term math although given the situation in the last years I have not seen a solid long term potential projection for Greece and certainly not one in 2014.

-

-

Posted by:

Thanks for the analysis.

1. Could you give some more insights on how you calculate the 10billion opportunity cost from the decline on economic growth?

2. What makes you include the drop in bank deposits at the cost in its totally? The drop does not seem not necessarily equate loss of wealth. Part of this money might be have been sent to foreign banks or remain hidden under mattresses. There is certainly a cost for the economy but adding it in its entirety seems unclear.

3. Providing the info on where the country's repos stand today is very illustrative. Do you have any data regarding where state arrears stand today?-

Posted by:

Thanks, 1) assuming the economy would have been 5% higher in the 2015-107 period 2) reduction in deposits is not loss of wealth, banks were put under severe liquidity pressure due to the deposit flight, had to resort to ELA and still try to recover from losing this volume of the deposit base and resume normal lending operations 3) arrears to the private sector have reduced from a combination of ESM funding for this purpose and making it a condition for disbursement, latest data is for Oct 2017 and they are 3.5bln

-