Podcast - Whose property? Greece’s housing challenges

Podcast - Whose property? Greece’s housing challenges Can the Green Transition be just?

Can the Green Transition be just? Where is Greek growth coming from?

Where is Greek growth coming from? Bravo, Bank of Greece

Bravo, Bank of GreeceWhere did all the money go?

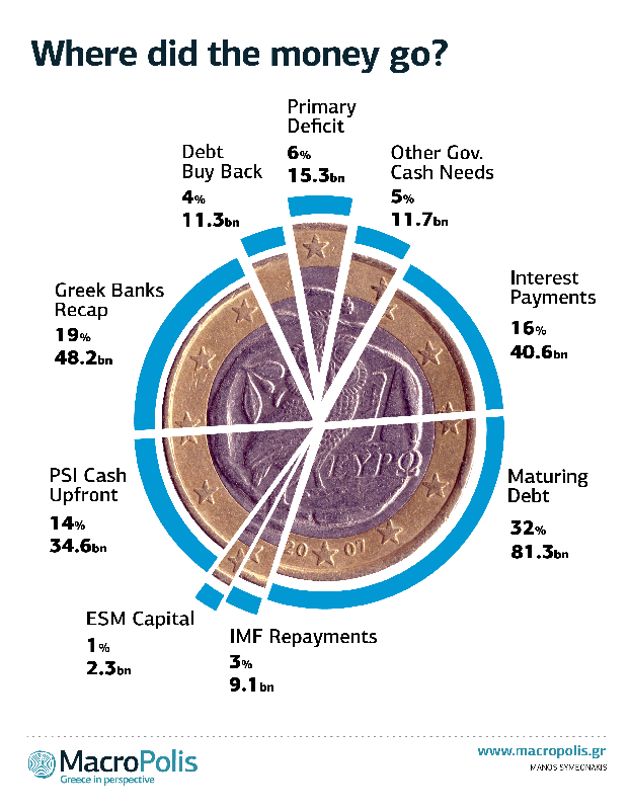

The total amount of loans the eurozone and the International Monetary Fund supplied to Greece between May 2010 and the most recent disbursements last summer stand at 226.7 billion euros. This is equivalent to almost 125 percent of Greece's economic activity in 2014.

The first programme was worth 73 billion euros, 52.9 billion of which came in the form of bilateral loans from eurozone members states. Another 20.1 billion euros was provided by the IMF.

The loans from the second programme agreed in March 2012 currently stand at 153.7 billion euros. The eurozone’s part is broadly completed as the EFSF has disbursed 141.8 billion with one last tranche of 1.8 billion remaining. The IMF has provided 11.8 billion of financing to date, with its involvement due to run to February 2016.

The combined eurozone involvement in Greece comes to 194.8 billion euros (107 percent of GDP), while the IMF total stands at 31.9 billions (18 percent of GDP).

These are staggering figures: No other nation has received this volume of loans in a period of 4.5 years.

From European Commission review documents, IMF evaluation reports, Finance Ministry budget documents and Hellenic Statistical Authority (ELSTAT) publications we pieced together roughly which financing holes this approximately quarter of a trillion euros closed.

Greece covered some of its financing needs during the period in question via a number of its own sources. The issuance of a 3- and a 5-year bonds in 2014 of 3 and 1.5 billion euros respectively, the increase of the stock of T-bills by 10 billion euros, the use of cash reserves of government bodies via repos worth 7 billion and privatization proceeds in the range of 2.4 billion, provided a total of 24 billion euros of own financing.

There seems to be a general misconception that feeds a misleading narrative in which the loans were used to keep the Greek state afloat, maintain its basic operations and pay salaries of doctors, teachers and policemen. Only last week Spanish Finance Minister Luis de Guindos made claims along these lines.

"Greece received 210 billion euros from the eurozone, including 26 billion euros for example from Spain," he said. “Thanks to this financing, which Greece could not get from financial markets, it was able to maintain all of its public services... to pay its doctors, its police, its retirees, thanks to this solidarity."

This is only part of the story, though. Indeed, Greece started the fiscal consolidation effort with a deficit before interest payments of circa 24 billion euros in 2009 and was running a primary deficit in 2010, 2011 and 2012. From 2013 onwards, though, revenues exceeded expenses and no financing was needed to cover state operations.

The brutal belt tightening meant that only just over 15 billion euros of troika loans were used for state operations. Combined with some other government financing needs (mostly relating to repayments of arrears that accumulated in the first two years of the crisis) the combined allocation to the Greek state’s operating needs was just 11 percent of the total funding, at circa 27 billion euros.

The financing breakdown speaks to the eurozone's objection to any form of debt restructuring at the very start of the Greek crisis. Roughly half of the financing was provided for debt servicing. From the loans, 81 billion was used to meet maturing debt obligations and for interest payments that exceeded 40 billion euros, almost 122 billion euros in total.

The second largest chunk of troika loans relates to debt reduction exercises. When lenders considered Greece sufficiently ring-fenced and core eurozone banks had reduced their Greek exposure, they decided to place the burden of the problem on private bondholders in February 2012 with the Private Sector Involvement (PSI). This was followed by the debt buyback in the end of 2012.

During the PSI, bondholders were offered new bonds with a face value equal to 31.5 percent of the face amount of those exchanged. They were also given sweeteners in the form of cash-equivalent EFSF notes maturing within 24 months for 15 percent of the face value of the debt exchanged. Also, they were offered short terms EFSF notes for the accrued interest. This totalled 34.6 billion euros or 14 percent of the combined financing needs.

An added 11.3 billion euros was used to buy back over 30 billion euros worth of debt in the second debt reduction initiative of 2012.

To support its banks from the losses incurred in the PSI and the rapidly deteriorating loan portfolios as a result of the deep crisis which saw non-performing loans soaring from 8 percent to 34 percent, Greece borrowed another 48.2 billion euros for bank recapitalisations, resolutions and the restructuring of the banking sector. An amount of 11.6 billion remains unused and could form the precautionary line of the eurozone after the end of the European side of the current programme.

The combined amount of the three initiatives reached 94 billion euros, more than a third of the total financing needs.

Greece started repaying last year the IMF loans supplied during the Stand By Arrangement of the first programme. A total of 9.1 billion euros was paid back by the end of 2014.

Greece also had to participate in the paid in capital of the European Stability Mechanism, to the tune of 2.3 billion euros.

The breakdown of how the programme funding was allocated clearly illustrates the crisis management strategy Greece’s lenders opted for. Eurozone leaders, with the reluctant agreement of the IMF, made a conscious decision to use almost two thirds of their “taxpayers' money” (as they like to refer to it) to service the debt which they refused even to reprofile at the beginning of the crisis, when it was essential and could have given Greece a chance of recovery.

To protect the integrity of the eurozone, the strategy has left Greece with a massive pile of debt and a quarter of the economy gone, still unable to stand on its own feet. It is this very debt and the pretence of key decision makers to present it as sustainable that keeps the country in a vortex of ongoing political instability, fiscal crises, troika fall outs and economic uncertainty. It is the magnitude of the surpluses required to maintain this sustainability pretence that in spite of the most phenomenal fiscal consolidation in ferocity and speed, Greece is still required to find savings in the volume of billions.

If the intention of eurozone leaders and institutions was indeed to keep their “boots on Greece's neck” due to the failings of its political class, as the ex-US Treasury Secretary Tim Geithner claimed in his book, they have achieved their goal. Now they need to be open about their own crisis management decisions and answer the uncomfortable question: Where did all the money go?

Follow Yiannis: @YiannisMouzakis

Sources:

European Commission - table 11 https://www.macropolis.gr/resources/toolip/doc/2014/04/25/ec_mou2_review_4_25-apr2014.pdf

European Commission - annex 4 https://www.macropolis.gr/resources/toolip/doc/2013/09/13/ec_mou1_review_3_february_2011.pdf

European Commission - Box 4 and table 19 https://www.macropolis.gr/resources/toolip/doc/2013/09/13/ec_mou2_march_2012.pdf

IMF - tables 4 and 5 https://www.macropolis.gr/resources/toolip/doc/2013/09/13/imf_mou1_review_3_march_2011.pdf

ELSTAT - table 12 http://www.statistics.gr/documents/20181/1234964/greek_economy_28_12_2012.pdf/9925c2b4-92ef-463a-8da7-2a44c8103ab3

ELSTAT - table 11 http://www.statistics.gr/documents/20181/1234958/greek_economy_24_12_2014.pdf/54f2cfe9-2b8a-4cb2-a738-52a89ccb838e

Ministry of finance (In Greek) - table 2.3 https://www.macropolis.gr/resources/toolip/doc/2013/09/16/mtfs_october_2012_greek.pdf

17 Comment(s)

-

Posted by:

Dear Yiannis,

unfortunately I failed retracing some of the exact numbers (Maturing Debt, Interest Payments, Other Gov. Cash Needs, Primary Deficit and Debt Buy back) given in your chart. I suspect they are combined by using Table Number 11 from The Second Economic Adjustment Programme for Greece Fourth Review – April 2014 and some other source I can't find. Could you please send me an overview of your calculation? I'm currently writing on a review of Yanis Varoufakis' Book "Adults In The Room" featuring a briefing of the euro crisis and the greek "debt" crisis in particular. In this context I'd like to include some your findings.

Thank you very much.

Heiko Schmid -

Posted by:

Are you acquainted with the financial term "Moral Lazard"? Everybody seems to forget that in capitalism, lenders, like all other participants, take a risk, and when they are not able to collect on some of their loans they need to regard their uncollected loans as a loss. But lately not in the EU or in the US. Banks can take all the risks they want and lend all they want without the implicit risk of losing credits, because they know that in the worst case scenario they will be bailed out by their governments. That is the implicit moral hazard that induces banks and corporations to take risky decisions, knowing they are covered. And who pays? The taxpayers of the countries indebted.

If we stick to free market logic, lenders must bear part of the cost for their risky business practices and borrowers must pay what they can if they can'`t pay as agreed. This is exactly what Argentina did. It paid its sovereign debt to the IMF and World Bank, but to private lenders it agreed to pay about 30 cents to the dollar to 93% of its créditors. They are stil fighting the vulture funds. But they avoided what is happening right now to the Greeks. That is why even the IMF is saying that Greek debt must be reestructured (namely reduce substantially) for it is completely unsustainable. -

Posted by:

So, a big chunk of the bailout money was used to roll over existing debt, i.e. to not let Greece default.

So? Why is that a big issue? What would the author rather have Greece do? Default? Greece deserves to default on it's debts so that Greeks find out about the consequences of such an action.

Honestly, I don't see the point of this analysis, nor do I understand the constant whining about the fiscal adjustment that Greece went through. Greece couldn't borrow through the markets, neither through it's own central bank like the "good old days", so it went through a big fiscal adjustment. I repeat, so? The alternative was to quit the euro and return to the drachma, but most agree that this is not desirable. If the author disagrees, he can say so clearly.-

Posted by:

Obviously they were going to be in trouble. the most basic rule of economy is borrowing should be the last resort, now i know that they borrowed to pay for what they borrowed. that is a very obvious nono! it is so simple. firstly they should never borrow 175% of their GDP! i would like to know what their original repayment plan was, cause otherwise i just think Greek government were con artists borrowing up to their necks and then planning to default all along. I feel sorry for the people, wish there was a way to help them out.

-

Posted by:

Following a few articles about the current debt crisis in Greece, I decided to google "how did Greece spend..." and this article came up. So, my understanding is still quite shallow, and I tend to oversimplify things, but it seems like there isn't much/any tangible policy going on. In other words, could they have focused more on microeconomics, encouraging small businesses and innovation? I know it's kind of too late anyway, but on a smaller scale, a loan could be repaid through earning the money and paying it back. What is "recapitalising" anyway? Do banks really need to be replenished? Could they have spent on more tangible things like tourism, accepting more international students at universities and exchange programs (rising Chinese middle class have money to burn), creating things people actually want/need, infrastructure, etc?

-

-

Posted by:

Congratulations! Your post was cited in the Belgian quality newspaper De STandaard, today:

http://www.standaard.be/cnt/dmf20150220_01541008 -

Posted by:

I sorry, but I think I you are so messed up. If I'm able to spend my own money in wages for doctors, professors, it is because someone is lending me money to spend on other things!!!!! Otherwise, I would not be able to do so: I would have to choose between paying wages or the other things!!!!

-

Posted by:

Hello. Have you taken into account the fact that T-Bill issuance increased from around €9bn in 2010 to €16bn in 2011?

-

Posted by:

If public debt is not increasing, then new issuance of debt (or new loans) will merely roll over (i.e., refinance) previous loans. Because Greek debt was already so high that it could not increase much, this is precisely what happened. So, this analysis is not surprising.

It is also worth remembering that Greece decided to increase its public debt, while other European countries just agreed to lend money on preferential terms (and can hardly be blamed for that). -

Posted by:

Brilliant analysis! Thank you.

-

Posted by:

Various articles in reputed western media have always made the point that most of the money graciously given to Greece has been used to avoid losses of big German and French banks that had been given (irresponsibly) for projects in Greece.

-

Posted by:

Dear Yiannis, thank you very much for that enlightening post. Could you maybe forward the raw data to me too? I am a German reporter and I am planning to write a post that deals with some aspects you touched here. Of course I will quote you properly.