-

Podcast - Brain Drain or Brain Regain? Understanding Greece’s Talent Flows

Podcast - Brain Drain or Brain Regain? Understanding Greece’s Talent Flows

-

The "King of the North" seeking to heal a fractured kingdom

The "King of the North" seeking to heal a fractured kingdom

-

How inflation has reshaped Greek household spending

How inflation has reshaped Greek household spending

-

Podcast - Shockwaves from the Gulf: What the Iran war means for Greece

-

Energy crisis puts squeeze on Greek fiscal policy

Energy crisis puts squeeze on Greek fiscal policy

-

Podcast - Kaisariani photos: Why Greece’s past is present

You've heard the Greek crisis myths, now here are some truths

There are certain truths about the Greek crisis. The main one is that Greece got itself into an utter mess by 2009. This came about as a result of two serious errors. Firstly, at a political and societal level there was an underestimation of the economic rigours of sharing a hard currency with more competitive and open economies, such as Germany and the Netherlands. The work needed in terms of public sector reform, tax collection, competition, productivity and exports was not carried out. Secondly, after a period of belt tightening to meet the criteria needed to enter the euro, Greek governments let go of the purse strings and never recovered control again. The dramatic fiscal derailment, particularly between 2004 and 2009, created an unmanageable public deficit and pushed Greece out of international bond markets.

At that point, Greece had two choices: To default or to seek a bailout. Another truth about the Greek crisis is that if it had defaulted, the economic impact domestically would have been severe and the absence of deficit financing would have prompted the need for abrupt austerity to close the deficit from year one. This approach would also have had a knock-on effect on many European banks holding Greek debt, which were already in a fragile position as a result of the global financial crisis. At the time, the eurozone did not have a defence mechanism and the strength of the financial integration in previous years would have become the single currency’s greatest weakness as the Greek crisis would have spread rapidly. In association with its eurozone partners, it was decided that a unique package of loans should be put together for Athens. This was deemed to be in the best interests of the eurozone as well as Greece.

At that point, the management of the Greek problem became a joint project. The successes or failures of the adjustment programme implemented in Greece from May 2010 have fathers of many nationalities, including Greek. The opening up of Greece’s domestic process to the outside world has given license to many people inside and outside the country to stand on the platform formed by the truths of the Greek crisis and dole out a number of myths that poison the relationship between Greece and its partners but also between Greeks and other Europeans.

Unfortunately, the election of a new government in Greece that, for better or worse, has a completely different view of how to handle its relationship with the eurozone has given rise to an increased peddling of myths about the Greek crisis from European decision makers.

Below, we seek to address some of these arguments, which are based on half-truths or falsehoods, and which have skewed much of the debate about how Greece and the eurozone should move forward.

Myth: The European taxpayer is footing Greece’s bill

Truth: The “European taxpayer” is a figure that has been near and dear to the heart of many crisis commentators, EU officials and politicians since early 2010. You will often hear references to the “European taxpayer” who has been bailing out the Greeks over the last five years. The same taxpayer has bailed out in similar fashion the Irish, Portuguese, Spanish and Cypriots but for some reason commentators and politicians seem to have particular issue with the “solidarity” provided to Greece.

Spanish Finance Minister Luis De Guindos has been one of the most frequent contributors to this debate over the past few months. He has claimed that Spanish taxpayers have forked out 26 billion euros for Greece. When one bears in mind that the EU contribution to the Greek programmes has reached nearly 200 billion euros and exceeded 120 percent of the Greek economy, it is quite easy for someone to create the impression that the “European taxpayer” has been bled dry by the profligate Greeks.

As is too often the case with the Greek crisis, reality is not exactly as it has been presented.

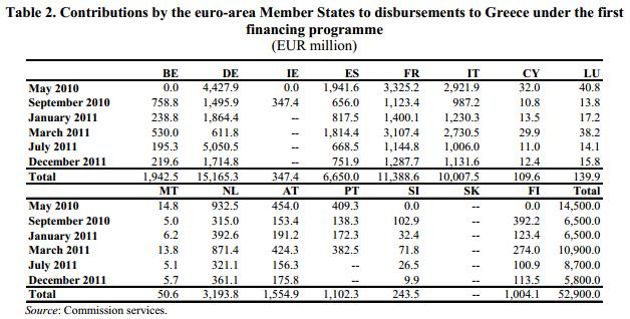

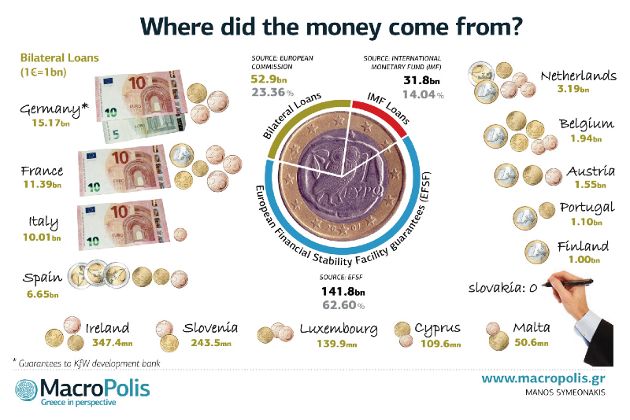

Between the end of 2009, when it was clear Greece was in trouble, and by the time the first Greek programme was agreed in May 2010, most of the time was spent by European leaders pretending there was not a problem and that a healthy dose of fiscal consolidation would restore confidence. They put together a mechanism to provide financing to an insolvent Greece based on bilateral loans being pulled together and managed by the Commission. This first package of 52.9 billion euros is set out in the table below.

This package did indeed consist of actual cash injections from eurozone members with the exception of Slovakia, which refused to participate, and Germany that provided guarantees to its AAA-rated development bank KfW, which raised the money through bond issuance. This means that German and Slovak taxpayers have not been burdened by the Greek bailout so far. Other member states did offer actual cash to Greece.

As a result of these loans, Greece owes 185 euros to each Finn, 118 euros to every Slovenian and 141 euros to every Spaniard. Greece also owes 15.2 billion euros to KfW, the German bank, but not to the German taxpayer. Interestingly, though, there is rarely a public admission that some of these countries have benefited from the “unintentional consequence of the crisis.”

By the time the second programme came into play, the eurozone had put in place the European Financial Stability Facility (EFSF), its own bailout fund, which was backed by guarantee commitments from member states, initially for 440 billion euros and then raised to 780 billion. The EFSF raised money by issuing bonds, so the “European taxpayer” only has a liability in the event of default of any of the fund’s investments.

The European Stability Mechanism was created in September 2012 and is different in structure because it actually contains paid-in capital which, after a round of increases, reached 80 billion euros in April 2014. Every single country contributed to the ESM, even those that were in a programme, as it is a eurozone-wide crisis fighting mechanism. Greece, for example, has contributed 2.3 billion euros to the ESM.

In summary, with the exception of the figures in the table above (and excluding Germany) these are the only figures that eurozone countries, and subsequently taxpayers, lent to Greece on a cash basis. The remaining 145 billion of loans from the EFSF should be of concern to the “European taxpayer” if, in 32 years time (which is the average maturity of the EFSF loans to Greece) or when interest payments start coming due, Greece is unable to pay.

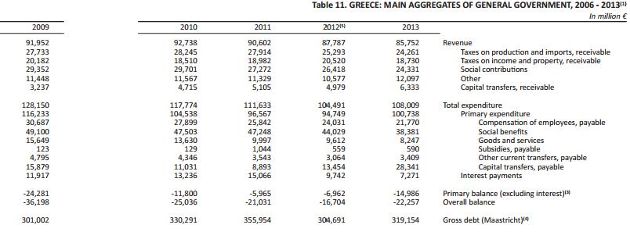

During these regular references to the “European taxpayer” and how generous he/she has been towards Greeks, EU officials have a habit of failing to be clear about what the money lent to Greece has been spent on. The result is many Europeans are left with the impression that their taxes have been funding Greeks’ pensions and salaries, when the truth is that only 11 percent of the 226.7 billion euros received by Athens has gone towards the government’s cash needs and covering the primary deficit, which no longer exists as of 2013.

Myth: What austerity? Greece needs to try harder

Truth: This brings us to the next myth about the Greek crisis that has resurfaced from time to time over the last five years and seems to be rearing its head again, which is that Greece has not been through a gruelling period of austerity or, as Portuguese officials have intimated recently, that Greece has opted for an “easy route.”

There could be a debate over the implementation of reforms in Greece since 2010 (although it should be noted that the troika, even belatedly, has signed off on the disbursement of all loan tranches until late last year). However, it is a mystery why anyone would consider that Greece has not done enough on the fiscal consolidation front. Unless, of course, they believe that there is a magic way to close a primary deficit of 10 percent of GDP (25 billion euros) other than to slash spending and raise revenue.

To wipe out this primary deficit in 2009 and reach a primary surplus of around 2.5 billion euros in 2014, three successive Greek governments had to take measures exceeding 30 percent of GDP.

When Greece’s insolvency was clear, Kostas Karamanlis’s New Democracy government had left a public sector wage bill of 30.7 billion euros, almost 13 percent of GDP. In 2013, that same wage bill did not exceed 21.8 billion euros, representing a 29 percent reduction in just four years.

Social benefits in 2009 had risen to 49.1 billion euros from 36 billions in 2006. This was brought down to 38.4 billion in four years, a 27 percent reduction.

The task was made even more difficult by the continuous reduction in revenues as people were losing jobs by the thousand each month.

To make this effort Sisyphean, the troika decided in 2012 to push down the minimum wage by 22 percent as part of the internal devaluation process. This reduced wages in all collective agreements and enterprise level wage decisions which used the minimum wage as a benchmark. In turn, this sucked tax revenues and social insurance contributions out of the system.

Contributions dropped from 30.7 billion in 2008 to just 24.3 billion euros in 2013, down 21 percent. At the same time, taxes on income were reduced to 18.7 billions in 2013 from 20.2 in 2009 in spite of the repeated revenue-raising measures that the governments introduced.

Given the magnitude of the effort and that the task was undertaken in an environment where a quarter of the economic activity disappeared while the labour force was also depleted by more than a quarter, it is ludicrous to suggest that there was something lacking in the fiscal consolidation effort. After all, this is an area of the Greek programme where the troika exercised its full authority and the numbers are there for all to see.

Myth: The programme is working: Exports are rising

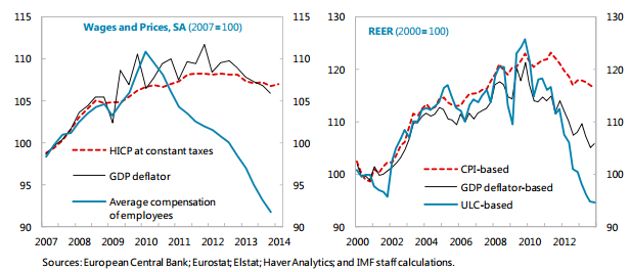

Truth: Another of the troika’s main objectives during the Greek programme has been to improve the country’s export performance by a process of internal devaluation and changing the economic model from one that was consumption-based to one that is export-oriented.

In the press conference that followed Finance Minister Yanis Varoufakis’s recent visit to Berlin, his German counterpart Wolfgang Schaeuble pointed to rising exports as one of the signs that the Greek programme is working. However, the Hellenic Statistical Authority (ELSTAT) shows that Greek exports fell by 1.4 percent last year.

One of the most comprehensive accounts on the performance of Greek exports is a report by the Organisation for Economic Cooperation and Development at the end of 2013. It is striking that the report found Greek exports were being held back in part by some of the policies the troika implemented with the intention of assisting them.

The share of Greek exports has been declining since 2008 and most of it is attributed to a sharp decline in services, mostly in maritime transport due to the slow pace of global trade and oversupply in the shipping sector since 2010. Equally, up to 2013 tourism revenues were badly hit by political uncertainty and certain eurozone partners questioning the country's euro membership, which peaked in 2012.

Competitiveness in prices, which the troika aimed to achieve through a sharp internal devaluation by the deregulation of the labour market, has not materialised even though in just 3 years Greece corrected all the labour cost competitiveness that was lost in the 2000-2009 period.

With Greece's exports concentrated in low-tech products (high-tech exports are only 28 percent of exports against a 50 percent OECD average) price competitiveness is of significance.

The lack of price adjustment compared to labour costs in parts reflects higher indirect taxes and public service charges as a result of the fiscal consolidation effort Greece is undertaking. The report finds that indirect tax increases pushed the cumulative effect of consumer price inflation by 6.25 percentage points between 2010 and 2012. If public service tariffs are also included the cumulative price push up is 9.5 percentage points.

The nature of the Greek economy, which is dominated by small- and medium-sized enterprises (SMEs) is also one of the factors that meant the price adjustments did not take hold. The OECD finds that 60 percent of the turnover is in the hands of SMEs, compared to 40 percent for the European average while Greek SMEs are half the size of the European SMEs. The weight of fixed costs that has been growing since the crisis started is affecting the capacity of small firms to adjust their profit margins.

Doing business is impeded by rising non-labour related costs resulting from difficult or expensive access to bank credit, supplier cutback of credit, long waiting times for VAT refunds from the state and delays in payments by customers, in many cases the state itself.

The OECD stresses that even in sectors that have been liberalised firms are forced to operate in very unfavourable macroeconomic conditions and the liquidity drain in the economy is impeding the entry of new players that will apply competitive pressures and push prices down,

The economic devastation experienced in Greece over the last five years is pushing some of those who have insist that the programme has been an equivocal success to clutch at straws. The policies followed to improve export performance should not be one of them.

Myth: Greece has to keep to its commitments

Truth: Over the last couple of weeks, European officials have been quick to stress that the new government needs to stick to the commitments made by the previous coalition.

Until now, Greece has abided by its bailout commitments. At times this has happened with great reluctance or much delay but fiscal targets have been met and reforms legislated. As mentioned before, whether much of this legislation regarding structural reforms has been implemented to full effect is open to question but the troika ultimately approved the disbursement of each loan tranche until last September, when the most recent review began and failed to result in an agreement, leaving 7.2 billion euros in instalments dangling. In fact, the OECD has found that Greece has been at the international forefront of structural reforms over the last few years.

Commitment, though, is a two-way street and Greece would be within its rights to accuse its eurozone partners of failing to live up to their commitments to Athens. On November 27 2012, the Eurogroup agreed to provide further debt relief to Greece once it achieved a primary surplus.

The relevant extract from the common statement on that day reads: “States will consider further measures and assistance, including inter alia lower co-financing in structural funds and/or further interest rate reduction of the Greek Loan Facility, if necessary, for achieving a further credible and sustainable reduction of Greek debt-to-GDP ratio, when Greece reaches an annual primary surplus, as envisaged in the current MoU, conditional on full implementation of all conditions contained in the programme.”

Despite this commitment and even though Greece achieved a primary surplus in 2013, a year ahead of schedule, no measures on further debt relief were offered. The previous government was told at the end of 2013 to wait until the primary surplus was rubber stamped by Eurostat in March. Then, it was told to wait until after the European Parliament elections in May. Then, it was told to wait until after the completion of the troika review that began last September. Greece’s lenders attempted to cover their reluctance with the fig leaf of claims that Greek debt was on a sustainable path.

Ex-Prime Minister Antonis Samaras must be vexed at hearing his former counterparts talk about “commitments” because one of the main reasons he finds himself out of office today is that the Eurogroup did not live up to one of the key pledges it made to him.

Instead, we find ourselves in a situation where Greece and the eurozone are at odds again, where stale arguments are being wheeled out to defend failures and where national interest on all sides is undermining the common currency. In this environment, the peddling of myths only impedes us from facing reality and tackling our problems together.

Follow Yiannis: @YiannisMouzakis

Follow Nick: @NickMalkoutzis

27 Comment(s)

-

Posted by:

Very helpful analysis. Especially the myth about the taxpayer. Thank you. Greece is still in, at this moment of time. 22/2/15. Don't leave us. Best of luck.

-

Posted by:

I don't thinks it's exclusively Greek to talk about Germany in such a way. I'm Irish and I also take a keen interest in all that is happening in Europe since the party ended and we woke to a horrible hangover. I'm no economic genius but the more I try and stand back to get a view of the big picture, the more Germany comes to the fore as reason there is so much European inequality. It has tried to impose itself with it's financial machinations and work ethics on different cultures. Granted, they do make good products. The % of their exports to GDP is enormous. A huge flood of money coming into the country. But they want more and more..

Greeks are a fun and friendly race. So are the Irish. Germans are dour and want to dominate.

Unfortunately, it looks like Greece needs to ask them for a favour because the other spineless European governments (including Ireland) are afraid to speak up against the schoolyard bully that Germany is. Maybe someday more people will see it. Or maybe their old friend Russia will be big enough to quieten the bully. -

Posted by:

First of all sorry for my bad English.

I am Portuguese and thank you for you enlightening article. Of course I review myself in it.

I would like to emphasize that I am ashamed of how my government has managed your struggle.

But what I want to know is this. In what stage is your energetic policy? Why Greece does not use your wealth in oil as trading currency and thus shut up the troika. Have Greece already tried to use it in the negotiations?

I wish to Greece the same as I desire to Portugal.

Be strong. Best of luck. -

Posted by:

Myth: in 2010 Greece was running a deficit of 15.8%

Truth: in 2009 Greece had a 7.8% deficit, but Germany insisted that had to be inflated!!!

http://hat4uk.wordpress.com/2012/06/26/greek-deficit-how-berlin-encouraged-papandreou-to-big-up-the-2009-greek-deficit/ -

Posted by:

Great article!

It should be translated to Greek if possible, especially the first part describing the "European taxpayer paying Greece's bills", because it seems there are still quite a few people in Greece believing this myth. The Greek mainstream media sell this myth every now and then. -

Posted by:

You've got the euro coins in the graphic mixed up between Germany and France. :)

Also, could you please address the KfW point in greater detail? Who bought the bonds? How do they work? Who is liable if Greece doesn't pay Germany back?-

Posted by:

Unless there was an edit, I think you missed the 5 Euro note tucked under the 10er in the German portion of the graphic.

-

-

Posted by:

All I have to say is thank you for this article. We need more of these because Myths exist especially abroad. I fight/argue every day with people here (Canada) who blame the Greek people calling Greek Lazy, not wanting to go work in the fields and produce fruits to export abroad, and not entrepreneurial enough to open up industries and employ everyone. Not honest tax payers, as if Income Taxes alone would solve the crisis. But what gets me most is the fact that there are those who accuse the people of Greece for causing the problem to begin with and which is utterly not true.

So thank you again for dealing with myths so people can shut up. -

Posted by:

"Whao"...go sell that to the EU..

-

Posted by:

Bottom line: kiss effing Merkel stupidity goodbye.

https://www.youtube.com/watch?v=nbI19ttJqWI

-

-

Posted by:

The major problem of Greece's adjustment program was, in my opinion, that it was never viewed by Greeks as 'their' program. Instead, it was viewed - probably with justification - as a Troika-program imposed on Greece and that Greece had no choice but to accept orders. It hurts to think what might have happened if George Papandreou had had a bit of Alexis Tsipras in himself as far as backbone vis-à-vis creditors is concerned.

The EU really had exactly zero experience with sovereign debt problems. True to form, they thought that sinners must be punished and acted accordingly. Had they known more about sovereign debt problems, they would have urged Greece to put together 'its' program which Greece would then have 'owned' and 'implemented' (obviously, with the Troika acting behind the scenes).-

Posted by:

Papandreou could not have pulled off a Tsipras. No politician of the old establishment would have had the public support to play the game Tsipras did. The consensus back home, even in the back of the heads of PASOK and ΝΔ voters, always was that Papandreou, Samaras, and co were a part of the problem, that they were the ones who caused all the mess. Tsipras has a fresh air which should last him a little bit -but not too long, and he knows it. If Europe wants to get the 'Greek problem' fixed, thay should also decide to move fast.

-

Posted by:

The proposed referendum in 2011 by Papandreou was a solution to this problem. Greek citizens would vote yes to a new program and in a way they would owned it. It is never too late for this.

-

-

Posted by:

When a country, like Germany, has to export more than 50% of its GDP otherwise it collapses then such country is a global threat.

If the US and Britain were to export the same % GDP as Germany, the world would be in a permanent state of depression.

Speaking about myths and truths here, the only truth you need to know is this:

Germany is a world pariah state whose insecurities and unsustainable economic model have created a persistent German problem for Europe since 1871 which remains unsolved and has plunged the world into two major wars and a third most destructive one soon to come.-

Posted by:

We don't want any favors. You are confusing people with government. We voted for them BECAUSE they said they wouldn't "ask for further favors". It's not our fault politicians once again lie.

-

Posted by:

It must be a special Greek way to talk about the country you want to ask a favour from as the root of all evil. Good luck with that

-